Indemnity caps in LMM: 10, 15, or 20 percent of price?

TJ Moruzzi

Published At Mon Jun 29 2026

Indemnity cap design decides how much of the purchase price the seller is actually keeping. The headline number on a press release is gross. The number after the cap, basket, and materiality scrape are applied is what the seller takes home if anything breaks in the first 18 months.

This post walks the practitioner ranges by deal size, the four basket types and how they interact, the materiality scrape question, and the survival periods that decide how long the seller's exposure lasts.

The TL;DR

- LMM indemnity caps run 10 to 20 percent of price for general reps, with smaller deals trending higher

- Fundamental representations are typically uncapped or capped at the full purchase price, with longer survival

- Basket types: deductible (most seller-friendly), tipping (middle ground), non-tipping (most buyer-friendly), mini-baskets (per-claim threshold)

- Materiality scrape: one-side scrape for breach determination only, two-side scrape for breach plus damage calculation. Seller wants one-side only

- Survival periods: 12 to 24 months for general reps, 6 to 7 years for tax and IP, longer for fundamental

- R&W insurance changes the calculus: cap drops to retention amount, escrow eliminated for general reps

What an indemnity cap is

The indemnity cap is the maximum amount the seller has to pay back to the buyer for breaches of representations and warranties after closing. It's the upper limit on the seller's post-close exposure.

A $30M deal with a 10 percent cap means the seller can be on the hook for up to $3M of indemnity claims. A 20 percent cap doubles the exposure to $6M. On a sub-$10M deal, it's not unusual to see caps at 25 to 30 percent because the buyer's coverage gap matters proportionally more.

The cap doesn't operate alone. It works in tandem with the basket (the floor before claims start counting) and the survival period (the time window during which claims can be made). All three numbers move together.

Cap by deal size

Practitioner ranges:

| Deal size | General rep cap | Fundamental rep cap | Survival (general) | |---|---|---|---| | Under $10M | 20-30% | Full price | 18-24 months | | $10M to $30M | 15-20% | Full price | 12-18 months | | $30M to $75M | 10-15% | Full price | 12-18 months | | $75M to $250M | 7.5-12% | Full price | 12 months | | Over $250M | 5-10% (often R&W) | Full price | 12 months |

Two patterns to notice. First, smaller deals have higher caps because the absolute dollar amount of exposure is smaller and buyers want bigger percentage cushions on businesses with thinner financials. Second, the gap between general and fundamental rep caps widens as deals get bigger.

Fundamental reps (corporate authority, capitalization, tax, ownership) almost always carry separate, larger caps because their breach is existential. A breach of "seller has good title to the assets" can unwind the entire deal. A breach of "the financial statements were prepared in accordance with GAAP" is recoverable through the cap.

The four basket types

The basket is the threshold of claims before indemnity payment kicks in. Four common structures:

Deductible basket

Claims accrue. Once aggregate claims exceed the basket, the seller pays everything above the basket. Below the basket, the buyer eats the cost.

Example: $300K deductible basket. Buyer claims $500K. Seller pays $200K. Buyer eats $300K.

Most seller-friendly. The basket acts like a true deductible.

Tipping basket

Claims accrue. Once aggregate claims exceed the basket, the seller pays everything from dollar one. Below the basket, the buyer eats the cost.

Example: $300K tipping basket. Buyer claims $500K. Seller pays $500K. Buyer eats nothing.

Less seller-friendly. The basket is a trigger, not a deductible.

Non-tipping basket (rare)

Claims accrue. Once aggregate claims exceed the basket, the seller pays everything from dollar one. The seller eats the basket too.

Example: $300K non-tipping basket. Buyer claims $500K. Seller pays $500K. (Same as tipping in this example, but if claims were $250K, neither party pays.)

Most buyer-friendly. Rare in LMM.

Mini-basket (per-claim threshold)

Each claim must exceed a per-claim threshold ($25K to $75K typical) to count toward the basket. Stops nuisance claims.

Often combined with one of the above structures. Example: $300K deductible basket with $25K per-claim mini-basket.

Basket sizing by deal size

| Deal size | Basket size (general) | Basket type | |---|---|---| | Under $10M | 1.0% of price | Deductible | | $10M to $30M | 0.75% of price | Deductible or tipping | | $30M to $75M | 0.5% of price | Tipping | | Over $75M | 0.25-0.5% of price | Tipping |

Mini-basket: $25K to $75K per claim, standard at most deal sizes.

The materiality scrape

Many representations include qualifiers ("material," "in all material respects," "to the best of seller's knowledge"). The scrape determines whether those qualifiers apply when calculating breach and damages.

Three options:

No scrape

Materiality qualifiers apply throughout. A "material breach" needs to be material to count. Damages are calculated only against material breaches.

Most seller-friendly. The seller's reps need to be materially wrong before there's any liability.

One-side scrape (breach only)

Materiality qualifiers apply when determining whether a breach occurred. Once a material breach is identified, damages include all losses (material and immaterial).

Middle ground. Seller's threshold for breach is high, but once crossed, damages are full.

Two-side scrape (breach and damages)

Materiality qualifiers ignored for both breach determination and damage calculation. Any inaccuracy is a breach, and all damages count.

Most buyer-friendly. Effectively turns "in all material respects" into "in all respects."

The seller wants no scrape or one-side scrape. The buyer wants two-side scrape. In LMM, one-side scrape is the most common middle ground.

Survival periods

How long after closing can the buyer make a claim? Survival periods by category:

- General reps: 12 to 24 months. Common range is 15 to 18 months.

- Fundamental reps (capitalization, ownership, authority): 6 years to indefinite. Often tied to applicable statute of limitations.

- Tax reps: 60 days after the close of the longest applicable statute of limitations (typically 6 to 7 years for federal income tax).

- Specific reps (employee benefits, environmental): typically 3 to 5 years, sometimes tied to statute of limitations.

The seller wants shorter survival on general reps. The buyer wants longer. The negotiation is between 12 and 24 months for general; the rest is fairly settled.

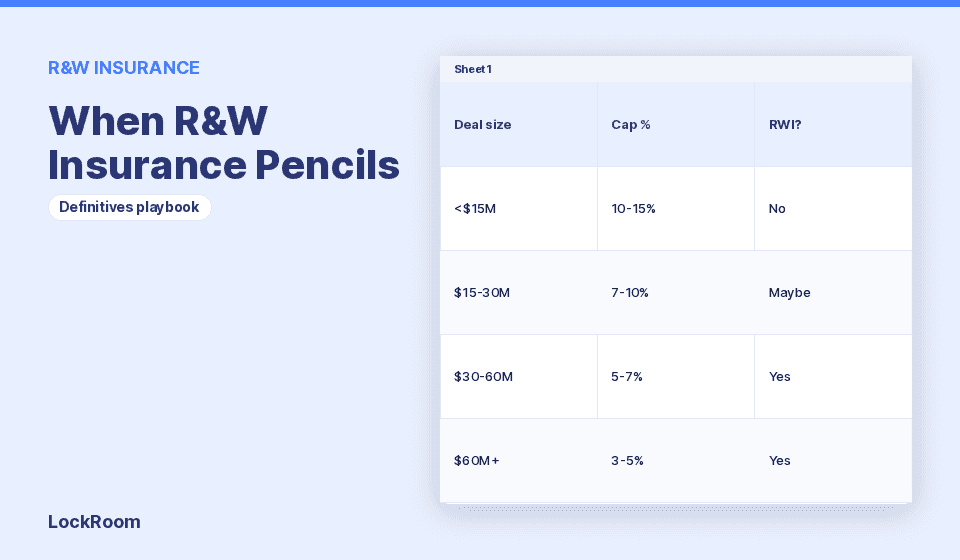

How R&W insurance changes the math

If the deal includes a buyer-side R&W policy, the indemnity package is restructured:

- General rep cap drops to the retention amount (typically 0.5 to 1.0 percent of price).

- Escrow for general reps is eliminated. Working capital escrow may remain.

- Fundamental reps stay outside the policy with the original cap and survival.

- Survival on general reps may shorten because the policy carries the long-tail risk.

For a $50M deal with R&W, the practical effect: $5M of escrow becomes $500K of retention. $4.5M freed up for the seller at closing.

For details on when R&W actually pencils, see the prior week's post on R&W insurance decision.

What buyers will push back on

Three areas where buyers consistently push for tighter terms:

- Cap level. Buyers anchor at 15 to 20 percent. Sellers anchor at 10 percent. Mid-deal compromise is 12.5 to 15 percent.

- Two-side materiality scrape. Buyers ask for it. Sellers refuse. One-side scrape is the typical compromise.

- Survival period. Buyers ask for 24 months. Sellers offer 12. Mid-deal compromise is 15 to 18 months.

Sellers who push back on all three save 5 to 10 percentage points of effective exposure on a typical deal.

Sample seller-favorable indemnity package

For a $30M deal:

"Indemnity Cap: 10% of Purchase Price for breaches of General Representations. Fundamental Representations: full Purchase Price. Specific Representations (Tax, IP, Environmental): full Purchase Price.

>

Basket: 0.75% of Purchase Price (deductible basket). Mini-basket: $25,000 per claim.

>

Materiality Scrape: applies for breach determination only. Damages calculated against actual losses.

>

Survival: General Representations 15 months. Fundamental Representations: indefinite. Tax: 60 days after applicable statute of limitations. Specific: 36 months."

This is an aggressive seller position but defensible at this deal size with a clean QofE and prepared data room.

Tools and references

For the LOI clauses where the indemnity package gets pinned, see the LOI Checklist.

For the working capital adjustment that often runs alongside the indemnity package, see the Working Capital Calculator.

For the earnout structures that interact with indemnity (some deals net earnout payments against indemnity claims), see the Earnout Structuring Matrix.

Bottom line

Indemnity cap, basket, materiality scrape, and survival period are the four levers that decide how much of the price actually stays with the seller after the first 18 months. The headline number is gross. The numbers below decide net.

Cap level is set by deal size. Basket type is the most-fought item. Materiality scrape is where buyers slip in two-side language and sellers should push to one-side. Survival is between 12 and 24 months for general reps, with 15 to 18 the typical compromise.

R&W insurance changes the math entirely. If the deal economics support it, the cap drops to retention and most of the exposure transfers to the policy.

Not legal advice. The indemnity package needs counsel review and customization for the specific deal.

FAQ

What's a typical indemnity cap in LMM? 10 to 20 percent of price for general reps, with smaller deals trending higher. Sub-$10M deals often see 25 to 30 percent caps.

What's the difference between deductible and tipping basket? Deductible: seller pays only the amount above the basket. Tipping: once basket is exceeded, seller pays from dollar one. Deductible is more seller-friendly.

What's a materiality scrape? A clause that ignores materiality qualifiers ("in all material respects") in the reps. One-side scrape ignores them for breach determination. Two-side scrape ignores them for breach AND damages. Seller wants no scrape or one-side; buyer wants two-side.

How long do reps survive? General reps: 12 to 24 months (15 to 18 typical). Fundamental: indefinite or 6 years. Tax: 60 days after statute of limitations. Specific: 3 to 5 years depending on category.

Does R&W insurance replace the indemnity package? For general reps, yes if the LOI is written to drop cap to retention. Fundamental reps stay outside the policy. Working capital adjustment stays outside.

What's a fundamental representation? Reps that go to the existence and ownership of the deal: corporate authority, capitalization, ownership of assets, no broker fees, sometimes tax and IP. They're treated separately because their breach is existential.

Can the seller cap exposure at less than 10 percent? Without R&W, hard. Below 10 percent, the buyer has limited ability to recover for material breaches. With R&W and cap dropped to retention, effectively yes.