LOI Checklist: A Free LMM M&A Reference

Clause-by-clause LOI guidance for LMM sell side deals. The 6 phrases buyers slip in, the 3 Term Lock framework, and rewrites that hold leverage on the seller side.

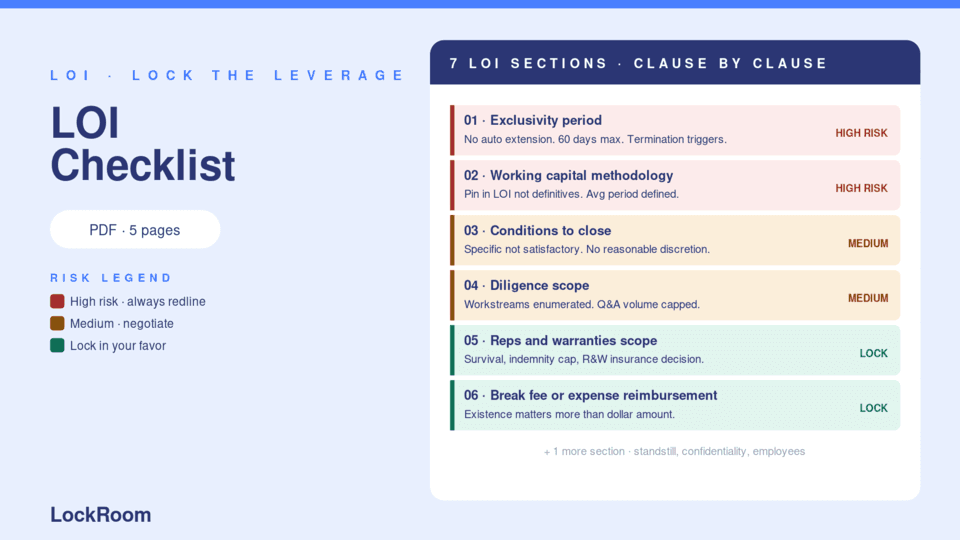

- 7 LOI sections covered clause by clause: exclusivity, price, conditions, diligence scope, working capital, reps and warranties, plus other

- The 6 phrases buyers slip in that quietly hand them retrade leverage, with stronger rewrite language for each

- The 3 Term Lock framework: lock the period, lock the price, lock the conditions

- Sample LOI redlines drawn from real LMM transactions

What's in the checklist

The PDF walks the LOI section by section. Each section lists what to look for, the phrases to redline, and a strong rewrite that locks leverage on the seller side.

- Exclusivity period — period length, automatic extensions, termination triggers, break fees

- Purchase price — firmness, working capital methodology, indebtedness definition

- Conditions to close — specific vs catch-all, financing, third-party consents

- Diligence scope — workstreams enumerated, customer call protocol, Q&A volume

- Working capital target — methodology, averaging period, true-up, dispute resolution

- Reps and warranties scope — survival, indemnity cap, basket type, R&W insurance

- Other terms — confidentiality, standstill, employees, closing logistics

Why this matters

An LOI is the document where most sell side leverage is won or lost. Sellers read the LOI once. Buyers read it five times.

The exclusivity period, the working capital methodology, the closing conditions: these are where a buyer builds the option to walk, retrade, or grind the seller down in week 8 of diligence. A clean LOI compresses diligence and holds price. A loose LOI invites the retrade.

See also The Earnout Structuring Matrix if the deal includes an earnout, and The Sell Side Diligence Prep Checklist for what to load in the data room before exclusivity starts.

The 6 phrases to always redline

- "automatically extending" in exclusivity

- "subject to satisfactory completion of due diligence"

- "at Buyer's reasonable discretion"

- "customary working capital adjustment"

- "in accordance with Buyer's standard methodology"

- Any exclusivity period longer than 90 days

Each one is small. Combined, they are the difference between a closed deal at the LOI price and a 12 percent retrade in week 8.

The 3 Term Lock framework

Lock the period. 60 days max. No automatic extension. Termination requires written notice. Cure period both ways.

Lock the price. Firm dollar figure or tight range. Working capital methodology pinned in the LOI itself, not deferred to definitives.

Lock the conditions. Each closing condition specific and objectively measurable. No satisfactory, no reasonable discretion, no customary.

If you cannot lock all three, you are not signing an LOI. You are handing the buyer an option.

Who should use the checklist

Sell side bankers reviewing buyer-drafted LOIs for the seller, especially solo bankers and small boutiques without an LOI standard internal template.

Founders negotiating directly with buyers without a banker, who need a clause-level reference to know what is normal and what is a leverage trap.

Sell side counsel reviewing LOIs for legal accuracy. The checklist surfaces practitioner-level commercial concerns that complement legal review.

Not legal advice. Have counsel review and customize before use on any specific deal.