MAC clause drafting in 2026: tighter than ever, and still buyer-favorable

TJ Moruzzi

Published At Mon Jul 06 2026

The material adverse change clause is the buyer's option to walk. It's also the most-contested provision in modern LMM definitives. After Akorn v. Fresenius made MAC enforceable as a buyer's exit, courts have continued to refine when a MAC actually gets a buyer out of a deal. The drafting matters more than ever.

This post walks the four elements of a MAC clause, the carve-outs that decide who's exposed to which risks, the quantified thresholds buyers want and sellers should resist, and the seller-favorable language that holds leverage during exclusivity.

What MAC is and why it matters

The MAC (sometimes MAE for "material adverse effect") is a closing condition that lets the buyer walk if something goes materially wrong with the business between signing and closing. It's the contractual answer to: "what if the business changes substantially during the gap between LOI and close?"

Without a MAC, the buyer is locked in regardless of what happens. With a loose MAC, the buyer has a near-unlimited walkaway right and the seller has effectively granted a free option. With a tight, well-drafted MAC, neither party has unilateral leverage. The risk allocation is explicit.

The MAC matters most in deals with:

- Long signing-to-close gaps (regulatory approval, financing, multi-jurisdictional)

- Customer concentration (one big customer churning could be a MAC)

- Sectors with rapid change (regulatory shifts, supply chain disruption)

- Recent earnings volatility

For a typical 60 to 90 day signing-to-close window in a stable LMM business, the MAC is theoretical. For a 6 month window in a regulated sector with concentration, the MAC is the deal.

The Akorn legacy

Before 2018, MAC clauses were almost never enforced. Buyers occasionally invoked them, courts almost always ruled against the buyer. The phrase "buyer's remorse" doesn't trigger a MAC.

Akorn v. Fresenius changed that. The Delaware Chancery Court found that Akorn had experienced a MAC and let Fresenius walk. The reasoning: Akorn's earnings collapsed during the gap, the collapse wasn't industry-wide, and the change was durationally significant.

Post-Akorn, courts started applying a sharper test. The MAC framework that emerged:

- The change must be "durationally significant" (not a temporary blip)

- The change must be substantial enough that a reasonable buyer wouldn't have signed at the agreed price

- The change must be specific to the target, not industry-wide

- The buyer can't have known about it at signing

That framework gave the MAC real teeth. Buyers started invoking it more often, especially in 2020-2021 (COVID-era deals where target performance dropped sharply). Sellers, in response, started drafting tighter carve-outs.

The four elements of a modern MAC

A complete MAC clause in 2026 has four elements:

1. The general MAC standard

The base definition. Standard language:

"Material Adverse Change" means any change, event, occurrence, or development that has had or would reasonably be expected to have, individually or in the aggregate, a materially adverse effect on the business, financial condition, results of operations, or assets of the Company taken as a whole.

This is the broad framing. It's deliberately vague because the carve-outs do the work of allocation.

2. Carve-outs

These exclude specific categories of events from the MAC. The seller wants broad carve-outs (events that don't count as a MAC). The buyer wants narrow.

Standard carve-outs:

- Industry-wide or market-wide changes (recession, sector decline)

- Regulatory or legal changes

- Geopolitical events (war, terrorism, pandemic)

- Changes in financial markets

- Acts of God

- Changes in GAAP or accounting standards

- Effects of the announcement of the deal itself

The seller's protection is the carve-outs. Without them, anything materially negative could potentially trigger MAC.

3. Disproportionate effect

Even with carve-outs, the buyer can still invoke MAC if the carved-out event affects the target disproportionately compared to industry peers.

Example: pandemic hits the sector. All companies suffer. Carve-out triggers. But if the target's revenue drops 50 percent while peers drop 15 percent, the disproportionate effect clause can revive the MAC.

The seller wants this clause limited or removed. The buyer wants it broad.

4. Quantified thresholds (optional)

Some MAC clauses include specific numerical triggers: "an EBITDA decline of more than 30 percent over a trailing 6-month period" or "loss of customers representing more than 25 percent of revenue."

Quantified thresholds are buyer-favorable when set low and seller-favorable when set high. They're useful in deals where the parties want certainty about what counts as a MAC.

In LMM, quantified thresholds are uncommon but appear in deals with concentrated customer bases or regulatory exposure.

Seller-favorable language

Three drafting moves that keep MAC tight:

Long carve-out list with no disproportionate effect clause

The strongest seller-favorable position: enumerated carve-outs (broad), no disproportionate effect modifier. This means industry-wide events never trigger MAC even if they hit the target hard.

Buyers rarely accept this in 2026. The disproportionate effect clause has become standard.

Time-limited measurement

Require that the MAC must persist for a defined period (e.g., 6 months) before it can be invoked. This filters out short-term shocks.

"Subject to subsection (b), an event shall not constitute a Material Adverse Change unless its effect persists for at least six (6) consecutive months."

Forward-looking certainty requirement

Require that the buyer demonstrate the MAC will continue, not just that it has occurred.

"Material Adverse Change requires both (i) actual material adverse effect on the date of measurement and (ii) reasonable expectation that such effect will continue beyond the closing date."

Buyer-favorable language

The mirror image:

Short carve-out list

Limit carve-outs to truly external events (war, pandemic, regulatory). Anything specific to the target's operations, customers, or financials is in scope for MAC.

Disproportionate effect with low threshold

"Disproportionately impact" with no specified percentage gives the buyer wide latitude.

Forward-looking impact (without certainty)

"Reasonably be expected to have" lets the buyer invoke MAC based on projection rather than realized impact.

Sample MAC clauses

Seller-favorable version:

"Material Adverse Change" means any change, event, occurrence, or development that has had a materially adverse effect on the business, financial condition, or results of operations of the Company taken as a whole that persists for at least six (6) months.

>

Excluded: changes in (a) the industry, (b) general economic or political conditions, (c) financial or capital markets, (d) GAAP or accounting standards, (e) law or regulation, (f) act of war, terrorism, pandemic, or natural disaster, (g) the announcement of this Agreement.

Buyer-favorable version:

"Material Adverse Change" means any change, event, occurrence, or development that has had or would reasonably be expected to have a materially adverse effect on the business, financial condition, results of operations, assets, prospects, or operations of the Company.

>

Excluded items not triggering MAC limited to: (a) act of war or terrorism, (b) GAAP changes. Any item disproportionately affecting Company relative to industry peers shall be considered a MAC.

The gap between these two is the negotiation. In LMM, the typical landing zone is somewhere in between, with broad carve-outs but a disproportionate effect clause that revives MAC if the target is hit harder than peers.

What the seller does at LOI

The MAC gets fully drafted in definitives, not LOI. But the LOI should include a placeholder that establishes the basic framework:

"Closing subject to absence of Material Adverse Change. MAC defined per market standard, with carve-outs for industry-wide, market-wide, regulatory, geopolitical, and announcement effects. Disproportionate effect clause limited to events affecting Company at greater than [X]x the industry-average impact."

Putting the framework in the LOI means the definitives drafting starts from a defined position rather than from buyer's standard template. For how the rest of the LOI allocates leverage clause by clause, see the LOI clause dissection.

What the seller does at signing

Before signing definitives, run a pre-mortem on possible MAC scenarios:

- What could happen between signing and closing that would materially affect the business?

- Of those scenarios, which are covered by carve-outs?

- Of the uncovered scenarios, which are the seller's responsibility (seller-controlled risk) vs the buyer's responsibility (post-close operational risk)?

- Are there specific known issues (pending lawsuit, customer review, regulatory inquiry) that need to be carved out by name?

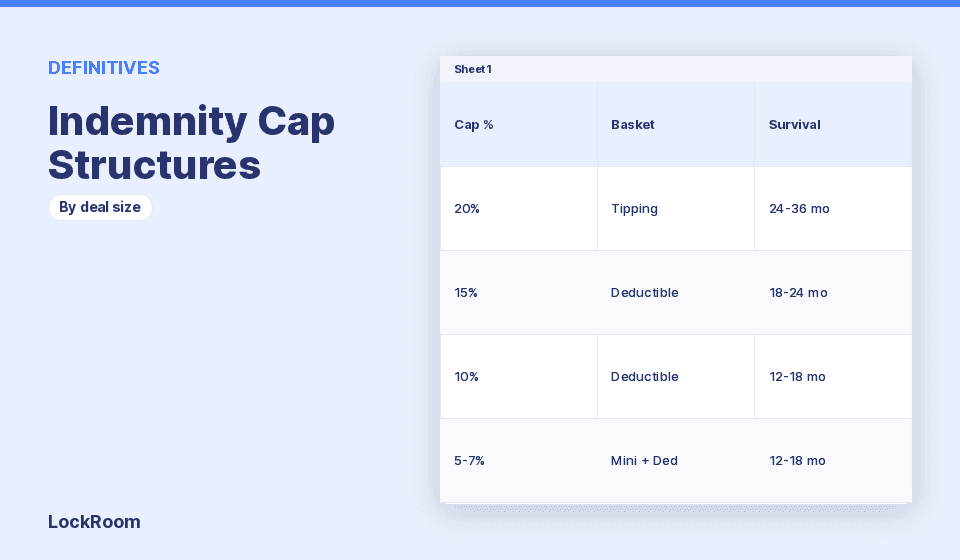

Specific known risks should be addressed in the disclosure schedule, not the MAC. The MAC is for unknown future events. Known issues belong in disclosed reps. How those reps are backstopped after close is a separate negotiation, covered in indemnity cap structures.

The 2026 trend

Two changes in MAC drafting since 2024:

Cyber MAC. Some buyers now insist on a separate cyber-MAC carve-in: a material cyber breach during the gap is a MAC even if it would otherwise be carved out. Sellers are pushing back, especially in non-tech sectors.

Pandemic and supply chain. Post-COVID drafting has explicit pandemic and supply chain carve-outs. The 2020-2021 wave of MAC litigation taught both sides that "act of God" wasn't specific enough.

Tools and references

For the broader LOI framework where the MAC gets initially scoped, see the LOI Checklist.

For the data room and diligence preparation that minimizes MAC risk by surfacing issues early, see the Sell Side Diligence Prep Checklist.

Bottom line

The MAC is a buyer's walk option. Drafting decides whether it's a meaningful protection or a buyer's free option to retrade in week 8.

Four elements: general standard, carve-outs, disproportionate effect, quantified thresholds. Sellers want broad carve-outs, no disproportionate effect, no quantified thresholds. Buyers want the opposite.

Post-Akorn, MAC has real teeth. Don't accept buyer's standard MAC language without redlining. Don't accept "or would reasonably be expected to have" without a forward-looking certainty requirement. Don't accept disproportionate effect without a defined threshold.

Not legal advice. MAC drafting needs counsel review and customization for the specific deal.

FAQ

What's the difference between MAC and MAE? None substantively. "Material adverse change" and "material adverse effect" are used interchangeably in modern definitives.

Can the buyer walk if the MAC is invoked? Depends on the contract. Most MACs are closing conditions: if MAC, buyer doesn't have to close. Some are termination triggers: buyer can terminate the agreement. The remedy structure matters.

How is MAC different from a closing condition? MAC is one type of closing condition. Other closing conditions include accuracy of reps, third-party consents, and regulatory approvals. MAC is the catch-all condition for unforeseen material change.

What's a disproportionate effect clause? A modifier to carve-outs. Even if a carved-out event happens (pandemic, recession), if the target is hit disproportionately compared to peers, the MAC can still apply.

Do quantified thresholds make MAC easier or harder to invoke? Easier for the buyer if the threshold is low. Harder if the threshold is high. Not commonly used in LMM unless there's specific concentration or regulatory exposure.

What did Akorn change? Akorn v. Fresenius (Delaware Chancery, 2018) was the first major case where a buyer successfully invoked MAC. It established that durationally significant, target-specific, substantial declines can constitute MAC. Pre-Akorn, MACs were almost never enforced.

Should the LOI include MAC language? A placeholder, yes. Specific terms get negotiated in definitives. The LOI should establish the basic framework (carve-outs, disproportionate effect approach) so definitives drafting starts from a defined position.