Covenants That Keep Deals On Track

The covenants between signing and close. Interim operating constraints, no shop and exclusivity, MAC clause carve outs. The provisions that decide whether the deal closes.

- Interim operating covenants explained: capex, compensation, customer contracts, ordinary course

- No shop and exclusivity language, including the fiduciary out carve out

- Material adverse change clause carve outs every seller should insist on

- How buyer overreach in covenants quietly hands the buyer a free option to walk

- When and how to negotiate definitives so the LOI work does not get given back

What's in the guide

The PDF covers the three covenant areas where most LMM sell side deals win or lose between signing and close:

- Interim operating covenants. What the seller can and cannot do with the business between signing and close.

- No shop and exclusivity. The seller's commitment to deal only with the buyer, with the carve outs that protect optionality.

- Material adverse change. What counts as material, what is carved out, and how to keep the buyer from walking on a market downturn.

Why covenants matter

The LOI sets the price and the framework. Definitives operationalize the framework. The covenants between signing and close are where the buyer protects the deal from surprises (legitimate) and parks optionality to walk or retrade (illegitimate).

Sellers who negotiate covenants carefully close at LOI price. Sellers who treat definitives as a paper exercise after the LOI hand the buyer free options that show up as walk threats or retrade demands in week 3 of the interim period.

See also The LOI Checklist for the framework that sets up covenant negotiation, and The Closing Checklist for the operational tasks during the interim period.

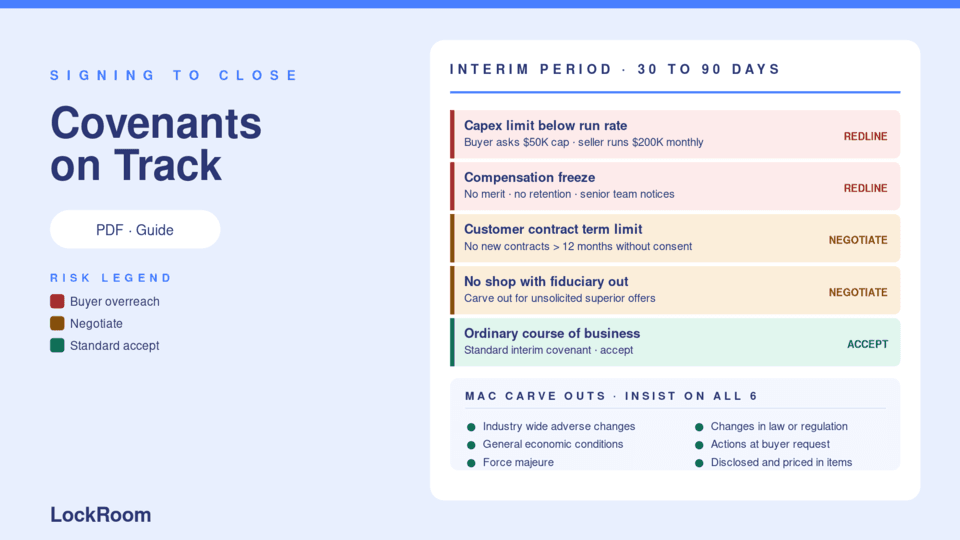

Common interim operating covenant overreaches

- Capex limits below run rate. Buyer asks for capex cap of $50K when the business runs $200K monthly. Sellers stop investing, the business deteriorates, the buyer renegotiates on the deteriorated business.

- Compensation freeze. Buyer asks for no compensation changes between signing and close. Means no merit increases, no annual reviews, no retention adjustments. Senior employees notice.

- Customer contract term limits. Buyer asks for no new contracts over 12 months. Means the seller cannot close the long term deals that drive the business.

- Vendor relationship freeze. Buyer asks for no changes to vendor relationships. Means the seller cannot replace a vendor that has missed delivery commitments.

- Hiring freeze. Buyer asks for no new hires. Means the seller cannot replace turnover, which by week 6 of interim creates capacity problems.

Each one looks reasonable in isolation. Combined, they freeze the business for the buyer's benefit while the seller carries the operational risk.

The MAC clause fight

The Material Adverse Change clause is the buyer's walk option if something material happens between signing and close. The fight is over what counts as "material" and what is carved out.

Carve outs every seller should insist on:

- Industry-wide adverse changes. If the entire vertical declines, that is not the seller's fault.

- General economic conditions. Recession, inflation, market volatility.

- Force majeure. Pandemic, natural disaster, war.

- Changes in law or regulation. New tariffs, new rules, new tax law.

- Actions taken at buyer's request. If the buyer asked the seller to do something and that thing causes a problem, the buyer cannot use it as a MAC.

- Disclosed items. Anything already disclosed in CIM, schedules, or diligence that has been priced in.

Without these carve outs, almost any negative news between signing and close becomes a MAC trigger. With them, the MAC clause is a backstop for genuinely material seller-specific events, which is what it is supposed to be.

Who should use this guide

Sell side bankers reviewing definitive agreements alongside seller counsel.

Founders approaching definitive negotiation who have not been through one before.

Sell side counsel looking for the practitioner-level commercial concerns that complement the legal review.

Not legal advice. Have counsel review and customize before use on any specific deal.