Sell Side Closing Checklist: A Free LMM M&A Reference

90 line items practitioners track from definitive agreement to wire confirmation. The punch list that keeps closings on schedule when every workstream converges in the final 30 days.

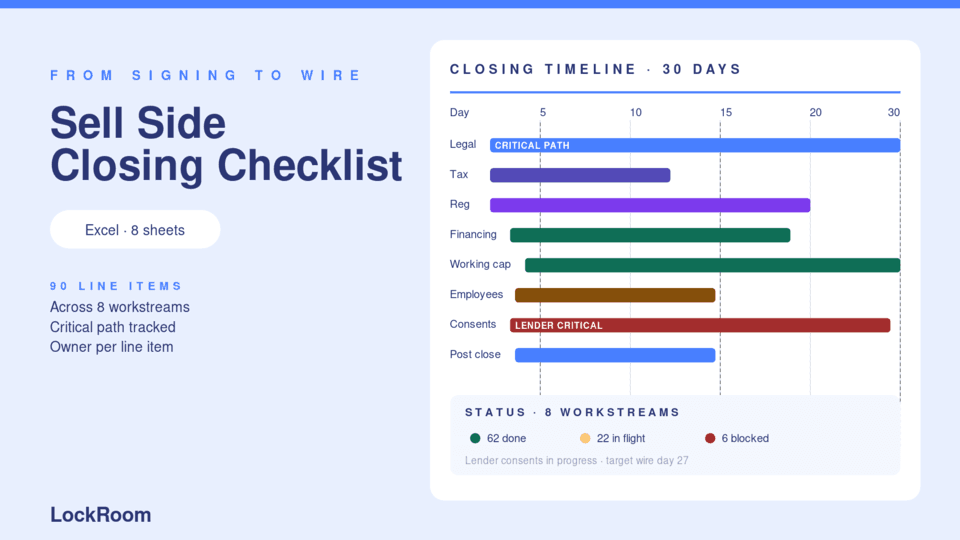

- 90 closing line items grouped into 8 workstreams: legal, tax, regulatory, financing, working capital, employees, third party consents, post close

- Owner column for every item (seller, banker, seller counsel, buyer, buyer counsel)

- Status, target date, completion date columns for tracking

- Pre populated 30 day timeline assumption with critical path identified

- Lender consent tracking with line by line by lender breakdown

- Working capital and net debt true up calculation methodology

The 8 closing workstreams

- Legal. Definitive agreement execution, ancillary documents, signatures, deliverables.

- Tax. Section 338(h)(10) elections, transfer taxes, sales tax filings, allocation schedules.

- Regulatory. HSR filings, CFIUS if applicable, state regulator notifications, industry specific approvals.

- Financing. Buyer financing confirmation, payoff letters for assumed debt, escrow funding.

- Working capital and net debt. Estimated calculation, target reconciliation, true up methodology lock.

- Employees. Notifications, offers, key person retention agreements, COBRA elections.

- Third party consents. Customer contract assignments, supplier consents, lease assignments.

- Post close. Wire confirmation, closing dinner logistics, transition services agreement activation, true up calculation start.

Why closings slip

Diligence is the front of the deal. Closing is the back. Most bankers and sellers underweight the back because the front is louder.

The reality: by the time the definitive agreement is signed, the buyer thinks the deal is done. The seller thinks the deal is done. Both are wrong. The 30 days from signature to wire are when one missed lender consent or one delayed regulatory filing slips the close by two weeks. The seller bridges the gap with another month of operating costs; the buyer rebooks committee meetings; momentum decays.

The checklist exists because closings are operational. Operational work fails when nobody owns each line. The checklist forces ownership.

The lender consent problem

The single most common reason LMM closings slip is lender consents on assumed debt or indebtedness exceeding the LOI cap. The seller's revolving credit facility, term loan, equipment financing, and any other debt instruments often require lender consent for change of control.

The checklist surfaces these in week 1 of closing prep. If a lender consent process takes 4 to 6 weeks (which is typical), starting in week 1 keeps the close on schedule. Starting in week 3 slips the close.

Symptom: in week 4 of closing prep, banker discovers the seller has a $2M equipment lease that requires lender consent for change of control. Lender takes 5 weeks to respond. Close slips by 5 weeks. Seller pays interest and operating costs through the gap.

Cure: line item on day one of the checklist. Identify every lender, send consent request immediately, parallel path with diligence completion.

Working capital and net debt true up

The closing balance sheet adjustment is where 1 to 5 percent of price moves at closing. On a $30M deal that is $300K to $1.5M. The methodology must be locked in the LOI; the calculation must be executed at closing.

The checklist includes the methodology lock confirmation, the closing balance sheet preparation, the dispute resolution process, and the true up payment timing. Most disputes happen because the methodology was loose in the LOI; the checklist surfaces this in week 1 so it can be addressed before closing.

Who should use the checklist

Sell side bankers running boutique LMM closings without a dedicated closing coordinator.

Sell side counsel coordinating with banker on operational closing items.

Founders who are the operational owner of the seller during closing prep, who need a single tracker for what is happening when.

Pair this with The LOI Checklist for the front of the process and The Working Capital Calculator for the closing balance sheet calculation methodology.