How to Win in Buyer Meetings

Pre-meeting preparation. The question playbook. The post-meeting follow up cadence that converts buyer interest into LOI.

- Pre-meeting preparation checklist for the seller and the banker

- The five themes every PE and strategic buyer probes during management presentations

- How to handle questions the seller does not have data for

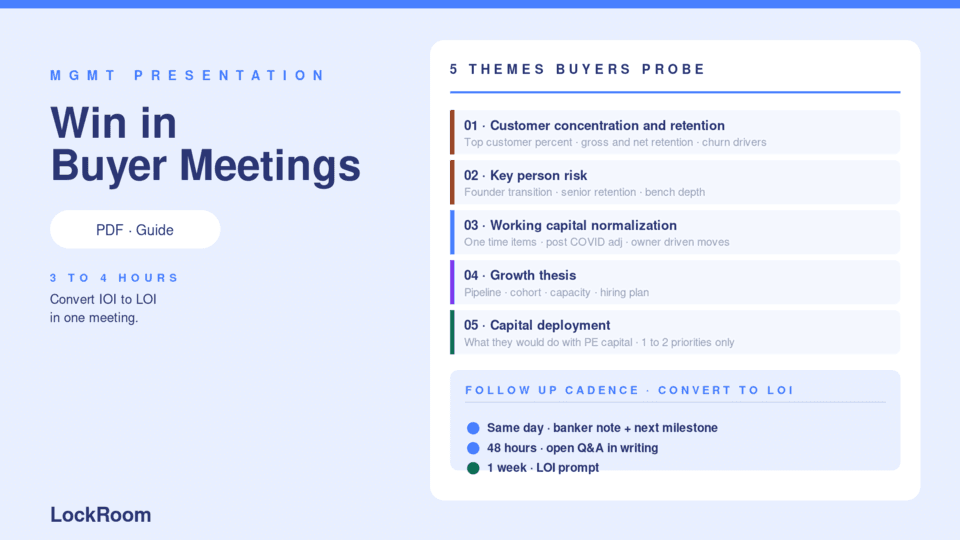

- Same day, 48 hour, one week post-meeting follow up cadence

- Why pitching synergies almost always backfires

What's in the guide

Buyer meetings (often called management presentations) are where IOI interest converts to LOI or quietly dies. The PDF covers three sections:

- Pre-meeting preparation. Who attends, what to rehearse, the document checklist for the buyer.

- The question playbook. The five themes every buyer probes and the prepared answers that hold up under follow up diligence.

- Post-meeting follow up. The same day, 48 hour, one week cadence that converts interest to LOI.

The five themes every buyer probes

Buyer meetings are not free-form conversations. The buyer's deal team has five questions they need answered before they will write an LOI:

- Customer concentration and retention. Top customer percent, top 5, gross and net retention, churn drivers.

- Key person risk. Founder transition plan, retention of senior leaders, depth of the bench.

- Working capital normalization. Any one-time items, post-COVID adjustments, owner-driven movements.

- Growth thesis. What backs the forecast. Pipeline, cohort, capacity, hiring plan.

- Capital deployment. The one or two things the seller would do differently with PE capital.

The seller who has crisp answers to all five wins LOIs. The seller who improvises through any of them gets dropped or retraded.

The "I'll follow up" rule

Sellers fail buyer meetings two ways. The first is failing to answer. The second, much more damaging, is improvising answers to questions the seller does not actually have data for.

The fix is verbal discipline: "I don't have that exact number with me. I'll get it to you in the post-meeting follow up." That answer preserves credibility. The improvised number gets caught in diligence and becomes retrade ammunition.

See also The Sell Side Diligence Prep Checklist for the data the seller should have ready before the first buyer meeting, and The CIM Template Outline for the document the buyer will be testing in the meeting.

Why pitching synergies backfires

Sellers often want to pitch the synergy case to strategic buyers ("you can cross-sell into our customer base, eliminate duplicate G&A, etc."). Almost always a mistake.

The strategic buyer's deal team builds the synergy case in their own model. If the seller pitches it, two things happen: the buyer discounts it (because the seller is incented to overstate), and the seller signals they are pitching the buyer's case for them. Both reduce price.

Let the buyer build the synergy case. Answer questions about the operational dynamics that enable synergies (margin structure, customer overlap, geographic footprint), but do not quantify the synergies for the buyer.

Who should use this guide

Sell side bankers running multiple LMM processes per year who want a tested framework for management presentation prep.

Founders preparing for their first set of buyer meetings.

CFOs and CEOs 6 to 12 months out from a process who want to start building the meeting muscle now.