Mastering M&A Leverage

How to hold leverage on the sell side. When and how to walk a buyer back, multi bidder dynamics in practice, and pacing tactics that work through exclusivity.

- When and how to walk a buyer back, with the credibility tests that make it work

- Multi bidder dynamics in practice, including IOI and LOI deadline staging

- Pacing tactics through exclusivity that prevent buyer-driven retrade

- How leverage shifts from seller to buyer the day exclusivity is signed

- Strategic vs PE buyer response patterns under genuine multi bidder pressure

What's in the guide

The PDF walks the three places leverage is won or lost on the sell side. It covers the tactics, the credibility tests, and the moments where most bankers and founders give the leverage back without realizing it.

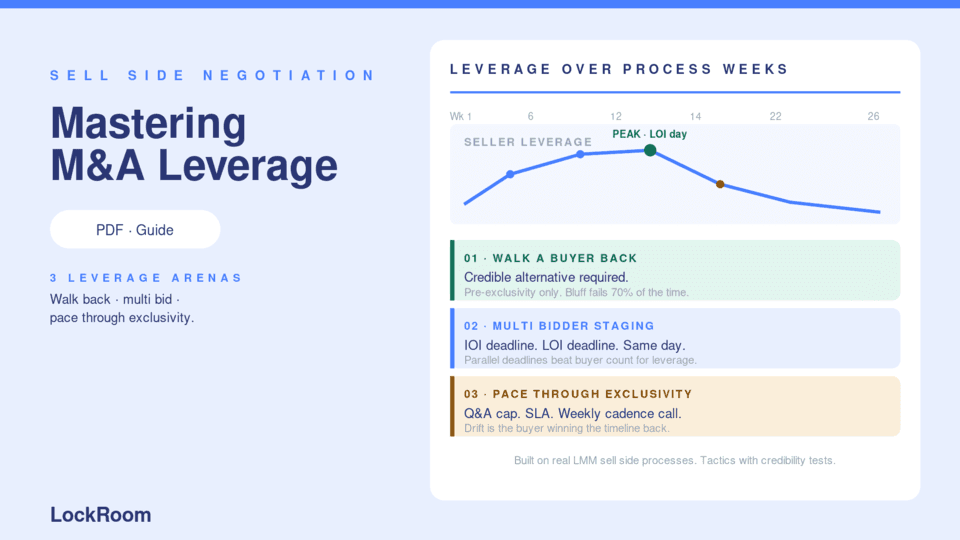

- Walking a buyer back. The disciplined removal of a buyer when terms slip. When it works, when it backfires, and the credible alternative requirement.

- Multi bidder dynamics. How parallel IOI and LOI deadlines create real leverage, not theatrics. Why staged deadlines matter more than buyer count.

- Pacing through exclusivity. The Q&A cap, the diligence SLA, the weekly cadence call. The mechanics of running the schedule rather than reacting to it.

Why leverage is mostly won before signing

Most sell side advisors think of leverage as a negotiation tactic. It is closer to a structural condition. The seller has leverage when alternatives are real and visible. The seller loses leverage the day exclusivity is signed.

Everything in this guide is built around that asymmetry. The IOI and LOI staging exists to keep alternatives visible. The Q&A cap exists to prevent the buyer from quietly extending the option. The pacing cadence exists to keep the seller driving the timeline.

See also The LOI Checklist for the clauses that lock leverage at signing, and The Buyer Outreach Tracker for staging multiple buyers in parallel.

The credible alternative requirement

Walking a buyer back works only when the alternative is credible to the buyer being walked. Two tests:

- Has the alternative buyer been disclosed at the right level? A second IOI in flight, a parallel mgmt meeting scheduled, a competing LOI received. The buyer should know the alternative exists, in detail, without naming names.

- Is the seller actually willing to walk? Buyers test the bluff by going quiet and letting the seller make the next move. If the seller folds first, the leverage flips and the price grinds down for the rest of the process.

Walking back without both is a one-time tactic that buyers spot and price into the next round.

How to stage multi bidder deadlines

The standard structure runs three buyer deadlines:

- IOI deadline (week 6). 6 to 10 buyers submit indicative offers on the same day. The seller and banker rank, give feedback, and invite the top 3 to 4 to management meetings.

- LOI deadline (week 12). 3 to 4 buyers submit final LOIs on the same day. The seller selects one for exclusivity. The other LOIs become the credible alternative for the next 60 days.

- Definitive signing (week 22). The exclusive buyer signs definitives. If the buyer retrades, the alternative LOIs (if still warm) become the option to walk.

The LOI deadline is the most leverage-rich moment in the entire process. It is the last day the seller has multiple parties bidding before exclusivity narrows the field to one.

Pacing tactics that hold leverage

- Q&A cap. 250 to 400 questions total, written into the LOI. Beyond the cap, the buyer pays for additional diligence dollars or the seller has cause to walk.

- Diligence SLA. Written response time commitments both ways. Buyer commits to 48 hour turn on key documents, seller commits to 24 hour turn on Q&A. Drift creates retrade ammunition.

- Weekly cadence call. Monday morning, banker leads, agenda is open Q&A items and upcoming milestones. The cadence call is where the seller drives the schedule.

- No open ended extensions. Any exclusivity extension requires written cause and a defined new end date. Open ended extensions are buyer optionality at seller expense.

Who should use this guide

Boutique sell side bankers running multiple LMM processes per year who want a tested framework for holding leverage through exclusivity.

Founders negotiating directly with strategic or PE buyers without a banker.

Sell side counsel reviewing process design and LOI structure for commercial leverage points.

Pair with Building Credibility and Control for the discipline that makes the leverage tactics in this guide actually work in practice.