M&A NDA Template: A Free Mutual Non-Disclosure Agreement for Sell-Side LMM Processes

Standard form covering confidential information, use restrictions, permitted disclosures, exceptions, and survival. For sell-side LMM teaser distribution.

- Mutual and unilateral variants with side-by-side clause comparison

- Standstill period and non-solicit carve-outs ready to drop in

- Redline notes addressing common buyer pushback

- Term and survival language that holds leverage post-LOI

What's in the template

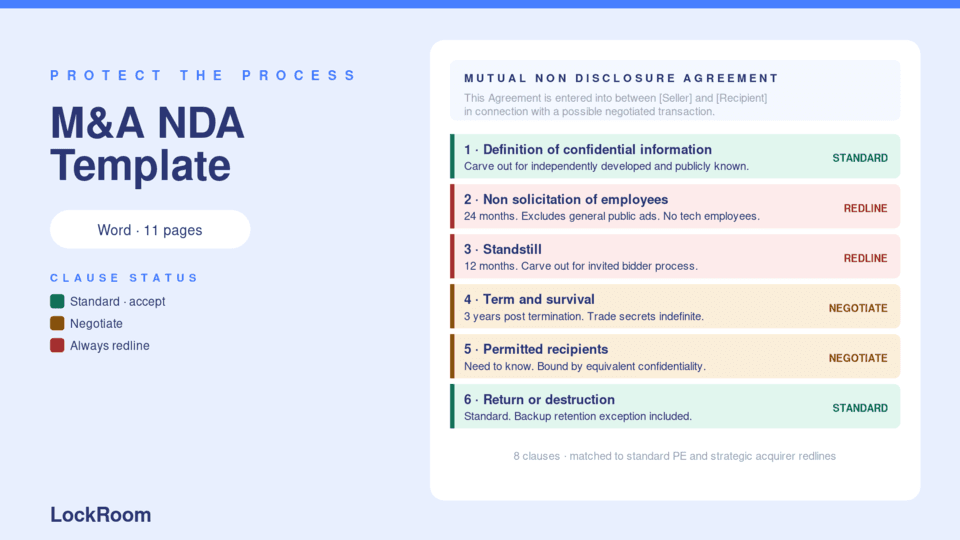

The 5-page PDF includes:

Front matter: How-to-use guidance, parties block, recitals.

Sixteen numbered sections:

- Definition of Confidential Information

- Use restrictions

- Standard of care

- Permitted disclosures (representatives, advisors)

- Exceptions (publicly available, prior knowledge, third-party rights, independent development)

- Compelled disclosure (legal process, subpoena)

- Term

- Return or destruction of materials

- Non-solicitation of employees

- No representations or warranties (subject to definitive transaction agreement)

- No license; no obligation to proceed

- Remedies (injunctive relief, attorneys' fees)

- Governing law and jurisdiction

- Assignment

- Notices

- Miscellaneous (entire agreement, severability, counterparts)

Signature block: Dual-side signature with name, title, date, email fields.

Notes page: Customization guidance, deal-specific variations, recommended workflow.

How to use this template

Step 1: Download the PDF and convert to your preferred editing format (Word, Google Docs).

Step 2: Fill in the bracketed fields highlighted in red italic:

- Effective date

- Discloser entity name, state of organization, entity type, address

- Recipient entity name, state of organization, entity type, address

- Term length (default 2 years)

- Non-solicit period (default 18 months)

- Governing law state and venue (default New York or Delaware)

- Signature block: name, title, date, email

Step 3: Decide on deal-specific customizations:

- Standstill clause: Omit for private LMM deals (already omitted in template). Add for public targets.

- Customer non-contact: Add a clause prohibiting Recipient from contacting Discloser's customers/suppliers without consent. Recommended for deals with significant customer concentration (see Customer concentration in the CIM).

- Term extension: Two years is standard. Longer (3-5 years) for highly competitive sectors. Indefinite for trade secrets.

- Non-solicit period: 18 months is typical. 24 months on competitive auctions.

Step 4: Have your counsel review before use on a specific deal. This template is a starting point, not legal advice.

Step 5: Use the template across all bidders in the auction. Uniformity is your protection. Bidders who counter-redline should be handled through your counsel.

Who should use this template

Sell-side bankers running LMM auctions who need a defensible mutual NDA to send to bidders before the CIM and data room access.

Founders doing direct outreach without a banker who need a starting NDA for inbound buyer interest.

Sell-side counsel drafting deal-specific NDAs from a known-good base template.

Buyers evaluating an inbound NDA from a seller's banker; the template shows what reasonable terms look like.

When to add a standstill clause

Standstills (acquisition restriction provisions) prohibit the Recipient from acquiring shares, making tender offers, or initiating proxy fights without the Discloser's consent. They are standard in NDAs for public targets but rarely needed in private LMM deals.

Add a standstill clause when:

- The target is publicly traded

- The seller has institutional shareholders concerned about hostile acquisition

- The Recipient is a strategic acquirer with public market activity

Skip the standstill (as in this template) for:

- Private LMM targets

- Sales to PE platforms or family offices

- Sales where the Recipient is the obvious natural buyer