Sell-Side QofE Scope Worksheet: A Free LMM M&A Reference

Provider brief checklist, EBITDA bridge requirements, working capital normalization scope, revenue quality, customer concentration. Bound the engagement before signing.

- Sell side vs buy side scope split workstream by workstream

- Provider RFP comparison sheet covering scope, timeline, and cost

- Timeline impact estimator so you know what you're buying

- Tax and commercial DD scoping language ready to send

What's in the worksheet

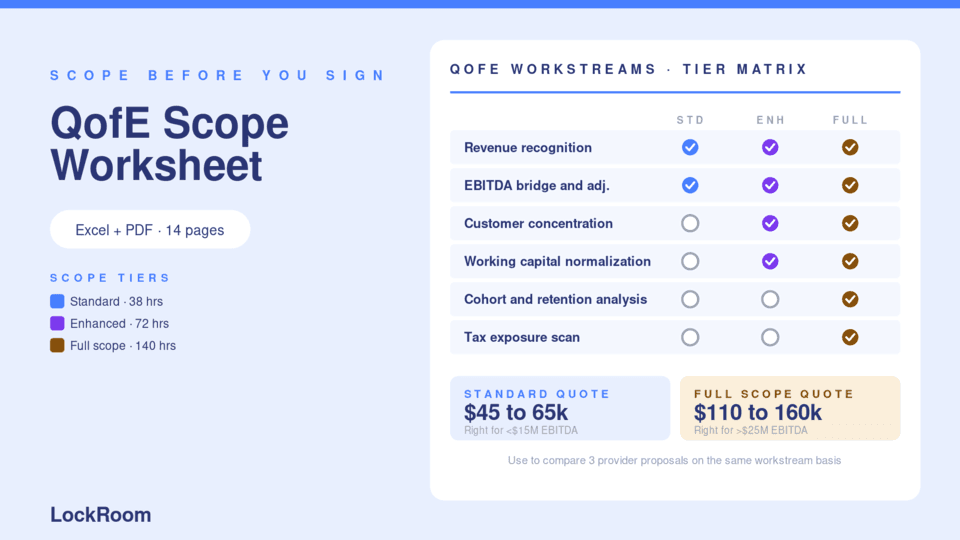

The PDF organizes QofE scope into 11 sections:

- EBITDA bridge and add-back analysis (CRITICAL)

- Working capital normalization (CRITICAL)

- Revenue quality (IMPORTANT)

- Cost of revenue and gross margin (IMPORTANT)

- Operating expenses and overhead (IMPORTANT)

- Capital expenditures and capitalization (IMPORTANT)

- Cash flow analysis (IMPORTANT)

- Debt and net debt items (IMPORTANT)

- Tax (IMPORTANT)

- Sector-specific items (healthcare, SaaS, manufacturing, professional services, distribution, insurance)

- Optional add-ons (three-statement model, customer cohort, vendor concentration, forecasting, benchmarking)

Each section has a numbered checklist for tracking what the engagement covers.

Plus:

- Provider selection criteria: three filtering questions and three questions to ask prospective providers

- Cost expectations table: boutique vs sector specialist vs Big-4 cost ranges with use cases

Why scoping matters

A QofE engagement's value is determined by scope. A poorly-scoped QofE that only covers EBITDA and working capital misses 60% of what the buyer's QofE will catch. The seller still gets retraded on the missing items.

A well-scoped QofE catches all six categories of typical findings:

- 40% EBITDA add-back disputes

- 25% working capital normalization

- 15% revenue recognition timing

- 10% customer concentration

- 10% other (capex, gross margin, deferred maintenance)

The worksheet's criticality ratings reflect this distribution. Critical items (EBITDA + working capital) drive 65% of findings. Important items cover the remaining 35%.

How to use the worksheet

Step 1: Pull this worksheet before talking to QofE providers.

Step 2: Use it to compare scope across providers. Ask each provider to mark which items they cover at their proposed price.

Step 3: Make sure all CRITICAL items are in scope. They drive the biggest retrade vectors.

Step 4: Add sector-specific items based on the target's industry. Healthcare deals need payer mix and billing audits; SaaS deals need ARR/NRR; manufacturing needs inventory deep dive.

Step 5: Negotiate optional add-ons based on deal complexity. A forecast review costs more but matters when the buyer is paying for growth.

Step 6: Use the provider selection criteria to filter to 2-3 finalists, then ask the three follow-up questions before signing.

Who should use the worksheet

Sell-side bankers scoping QofE engagements for sellers preparing to launch.

Founders evaluating QofE provider proposals and understanding what the engagement should cover.

CFOs working through QofE prep and ensuring their internal data is ready for what the provider needs.

Buyers building their QofE scope; the worksheet shows what a comprehensive scope looks like.

Provider tier guidance

Boutique advisory ($20K to $45K): Most LMM deals ($5M to $50M EBITDA). Recommended for the vast majority of LMM processes. Examples: Embarc Advisors, Calder, Bonadio Group, Frazier & Deeter. Partner-led engagement, sector experience, faster timelines.

Sector specialist ($40K to $80K): Healthcare (Pinnacle Healthcare Advisory, Stout Healthcare), SaaS-focused providers, financial services-focused providers. Sector expertise integrated with financial QofE. Worth the premium when regulatory or sector-specific complexity is high.

Big-4 / national ($50K to $150K): Deloitte, EY, KPMG, PwC, Grant Thornton, BDO. Used when the seller anticipates an upper middle market buyer who expects a recognized name on the report. Brand recognition and deeper data analytics, but for most LMM processes the boutique tier produces equivalent quality at a fraction of the cost.